Recently, the Ontario Education Minister, Mitzie Hunter announced that the ministry of education will start to roll out a pilot financial literacy project for 28 high schools in Ontario. This project aimed to teach our grade 10 students about money and to provide them with more financial literacy. When I read the article, I was excited to hear that our provincial government had finally recognized that financial literacy and money skills are important to our society and it should be taught in our schools. However, what exactly will be the curriculum of this new financial literacy course is still unclear. So instead of waiting for the government to come up with the new curriculum, I’ve come up with a list of topics that I think will be relevant to the average Canadian. I would also want my kids to have the exact financial literacy when they grow up.

Credit History, Report And Score

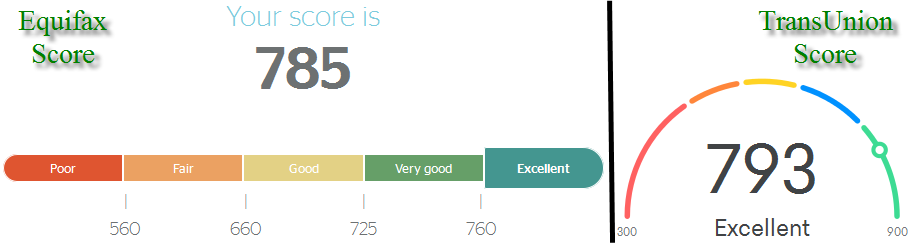

Before applying for my first mortgage, I have no idea what is credit history. How do I build my credit history? Who stored information related to my credit history report and how accurate? What credit score is considered to be a good credit score? When should I start building my credit history? Why is my credit history important? These are all important questions that I wish I knew before I purchased my first home. It may have affected the mortgage rate I was offered and could have cost me thousands of dollars in interest payments. Hence, credit history management should be a part of the financial literacy curriculum.

Basics About Borrowing

Ever since I could remember, borrowing money from financial institutions to purchase material possessions that we don’t yet have money to pay for seems like a norm in the developed countries. Having the basic knowledge with regards to secured and unsecured personal line of credits, home equity line of credits, mortgages, student loans, car loans, credit cards loans, installment loans and payday loans is crucial. The average Canadian needs to know what is the effective annual interest rate for all the different loans. When does each type of loan start incurring interest? Which type of loans offers the best borrowing rate? How to qualify for the different types of loans? By knowing the lowest borrowing cost and being able to compare the different types of loans will provide the average Canadian with a great foundation to build his/her financial health on.

Filing Your Income Tax

There are only two certainties in life: death and taxes. Pop quiz. When do you have to file your tax return? Is filing your income tax mandatory even if you don’t have any income for the fiscal tax year and you are in the age of majority? Are there any benefits to filing your taxes? How do I pay less income taxes? Are there any special tax credits that I can apply for when I file my tax return? Do I need a tax accountant to file my income tax? These are the basic tax questions that every Canadian should know. Second pop quiz. Do you know that even on the year of your death, you still have to file your income tax? Well, you can’t because you’re dead. However, whoever manages your estate will need to file your last income tax return on your behalf. If every Canadian have to file his/her income taxes until death, shouldn’t it at least be a part of the financial literacy curriculum and be taught in school?

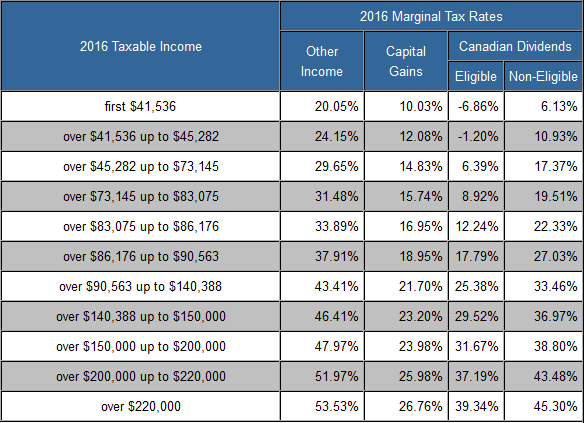

Sourced from TaxTips: Ontario Marginal Tax Rates

Income Tax Brackets

The income tax system in Canada is progress, which means the more you earn, the more tax you’ll pay. A while ago, I read a story about a fellow who refused a pay raise because the pay increase will push his income into a higher tax bracket. My jaw dropped when I finished reading that story. I started to wonder and I asked myself “how many Canadians had the same misconception as this poor fellow when it comes to the Canadian tax system?” Suffice to say, the financial literacy curriculum requires a dedicated section for the tax system to educate Canadians how their incomes are being taxed.

Tax Efficiency For Different Income Sources

When I first learned about the Canadian tax system, I became aware of the three major categories of taxable incomes: employment or self-employed income, dividend income and capital gain income. For the employment or self-employed income, every dollar you earned is being taxed. There is no way around it, so this form of income, you pay the highest amount of tax. For the dividend income, it’s grossed up, which means they’ll add an additional amount on top of the dividends that you received. Your taxable income will be increased by that amount. However, you will also get a dividend tax credit. Based on the tax bracket chart above (for Ontario residents), if you earn $90,563 or less for the tax year of 2016, dividend income will be your least taxed form of income. Last but not least, the capital gain income is only taxed at half the amount. For example, if you made $10,000 in capital gain income, then only $5,000 will be added to your taxable income. Even though I have covered the basics, how to differentiate which form of income falls into which category need to be fully covered by the financial literacy curriculum. Check out this post if you are interested in minimizing your income tax.

Registered Retirement Saving Plan (RRSP)

A couple of weeks ago, a friend of mine called me up to ask about the spousal RRSP rule. He’s a high-income earner with very little RRSP contribution room left for the 2016 tax year. On the other hand, his wife’s 2016 income was lowered than his and she had quite a bit of RRSP contribution room left as she rarely contributed to her RRSP. My friend thought that if he contributed to his spousal RRSP account, he’ll be able to take his wife’s contribution room for the same amount that he contributed and lower his income by that amount. However, that’s not how the spousal RRSP account works and the RRSP contribution limit is not transferable. This is just a simple case of misunderstanding of the use of the spousal RRSP rule. With that being said, there are many more RRSP related rules that the average Canadian needs to know. By adding a section related to the financial literacy curriculum, all Canadians will have the basic knowledge to reap the benefit of the RRSP when they retire.

Registered Education Saving Plan (RESP)

A lot of parents are working very hard to save for their children’s future post-secondary education by contributing $2,500 annually to the RESP account to get the government’s $500 education savings grant per child. Some parents even think that they need to have one RESP account for each child. Actually, there is a family RESP account that can have multiple beneficiaries. Any kid under the age of 18 in anyone’s extended family can be a beneficiary of the RESP family account. In addition, anyone can contribute to the family RESP account, but the contribution limits and government education savings grant still applies for each individual beneficiary in the account. Since the majority of the general population will get married and have kids one day, having an RESP category as part of the financial literacy curriculum seems like a logical choice. Here is a very thorough and well-written RESP article by Mike Holman

Tax Free Saving Account (TFSA)

Do you know that the Tax Free Saving Account may get taxed? Surprise? You’re not alone. For the individuals that over-contributed to their TFSA, they will be levied a 1% tax for each month on the amount over their contribution limit (either lifetime or annual). Since the TFSA was only introduced during the last major financial recession in 2009, it’s still relatively new and mysterious comparing to the RRSP and RESP programs. To ensure that the average Canadian can fully benefit from saving to this account, the financial literacy curriculum should consider adding a section for the TFSA.

Canadian Pension Plan (CPP)

In all honesty, I have very little knowledge of the CPP. I have always had this fear that the baby boomer generation will be depleting most of the CPP resources when they retired. The baby boomer generation does represent a significant portion of the population after all. With such a large portion of the population going from being contributors to recipients and not enough new blood to replace them, I don’t think that the CPP program is sustainable. I hope that I am wrong in this aspect so I can get in line to get my share of the CPP benefit when I retire. I have been contributing (not by choice) to the CPP every year since I joined the workforce. Some of the major questions that I have and still need answers to, are: what are the maximum CCP payment that I can get? At what age can I start receiving the CPP benefits? If I have an employer pension plan, how does it affect my CPP benefits? Can I get a lump sum instead of a monthly pay cheque? I would love to attend this section of the financial literacy curriculum when they offer it.

Old Age Security (OAS)

Another black box to me. I don’t have the confidence in any of these government programs when I retire. My fears may be overblown, but I don’t want to be at the mercy of any politicians’ hand out when I retire. This is why I work so hard to save money to ensure that I retire on my own terms. With that being said, I still need to know how my own income after retirement can affect the amount of money that I get in OAS payments. I don’t have any hope of getting any OAS payments, but if I get any, it’s going icing on my retirement cake. Once again, I would love to attend this section of the financial literacy curriculum when they offer it.

My Two Cents

Depending on how you look at it, this may be an exhaustive list or just a skim of the financial literacy curriculum surface. I’ve always believed that our school system lacked the financial literacy curriculum to prepare our kids with the required money skills to manage their finance effectively, efficiently and most important of all, responsibly. I hope that this post will motivate the average Canadian to push the governments harder to provide more financial literacy curriculum in our school system. In addition, if you don’t have basic knowledge of all the topics that were covered in this post, I’d encourage you to start your financial literacy journey. I really need someone to kick me from behind for lacking knowledge in the CPP and OAS area and start learning more about these two topics.

About Leo

About Leo

Morning Leo, It’s about time isn’t it!

Its honestly so dumb it took this long, Im guessing its because Canadian’s are at all time high debt levels.

I have never really used algebra, but finances we use daily. I agree with you about the Canada Pensions Plan. Hopefully there is still something left once we retire. Dave Ramsey has been helping schools in the U.s teach students about money, seems to be helping them. Sometimes the government can surprise ya and do something right!

@PassiveCanadianIncome, It’s not that I don’t have faith in our wonderful government, but they have not demonstrated to be able to manage public funds responsibly. Here a are a few examples, the Ontario government wastes billions every year on the botched hydro system, the Toronto Transit Commission can never balance a budget and city councilors voted for their own pay increase. Now you can see why I am counting on my own funds for retirement.

I agree with your statements…. financial literacy is lacking all over the world and it’s up to us to help!

It’s kind of funny how you have people in politics who are setting budgets but might not know how to set them for their personal life. It’s like the fat guy giving you advice on how to get fit 🙂

@Erik, this post is almost like an open letter to the government asking them to do more on the financial literacy front. I see that governments are spending quite a bit of money running programs like opening drug addiction centers or legalizing marijuana. So why not spend some money to provide financial literacy that can benefit everyone in our society?

So true! It is the same here in the Philippines. People pay for stuff (even education, how ironic) thru loans then are enslaved to pay debts, tax, then it becomes a vicious cycle crippling more and more.

@Shaun, you’re definitely right about the debt cycle. Too often, people don’t understand how some debt works and they carry a balance with high interest debt such as credit card debt. This is a wealth destroyer and I don’t recommend anyone to carry a balance on their credit card debt. If you can’t pay your credit card bill in full every month, then use cash.

I think this is a great idea that needs more attention in schools. I never attended school in Canada (I’m originally from the States) and there really isn’t much like this there either. I mean, they teach you about budgets and call it a day basically. I can’t remember the last time I used a lot of algebraic junk in my life, but I sure did struggle with finances for years. I would love to see in be added into school curriculum all over.

@Jessica, there is definitely a need for financial literacy all over the world. All young people need to be aware that their lives revolve around everyday finance and they need to know the impact of their decisions. Hopefully, there will be more people advocating for more financial literacy with their local government.

I think that we as parents need to teach our kids about money from an erily age. I would be so ashamed if my kids started applying for Quick cash loans when they’re adults

@Viktoria, as a parent of two young kids myself, I am starting to teach them about money as soon as they know what money is and how our lives are revolving around money. The earlier they learn about the value of money and money concepts, the better.

Excellent financial literacy topics – useful for those who may not have this taught at school. I know Malaysian schools are still far behind when it comes to financial literacy. My friends who are parents have to teach them themselves.

@Emily, until I see exactly what’s in the curriculum of the financial literacy course, I will not be depending on the school system to provide my kids with the basic financial literacy that my kids will need. Raising financially responsible kids is a high priority for me.

I’m not Canadian, but I still think these are all ideal topics for financial literacy. Some of these are even things I’ve already started working to teach my teenager (she just turned thirteen). It’s amazing how many people don’t seem to think kids need to learn this stuff, so I think it’s great that they’re going to be teaching it to the kids in your area.

@Brandi, it’s great that you are teaching your kids money concepts. My believe is that all kids need to enroll in some basic financial literacy course in their school. The earlier, the better.

loving all these valuable tips shared… it is definitely a must read for all….

@Miera, thanks for dropping by and visiting my site.

Wow, this is so relevant – even for those of us outside Canada. Understanding money and finances is so important as an adult. I only wish that financial literacy was taught to me when I was in high school!

@Chloe, After I graduated from University, I felt lost financially and had $30,000 of student loan. Fortunately for me, I discovered that early enough to avoid the deadly debt cycle. Creating financial literacy awareness is actually one of the reasons why I started my blog.

I think it’s fantastic that Canada is tackling Financial Literacy. Especially in the school system. We don’t have anything like that down here in Florida. But, we’ve taken it upon ourselves to educate our kids on some of the basics. And on our views of money and debt.

@Becki, kudos to you for recognizing that your local school system is not providing sufficient financial education to your kids and taking the rein to ensure that your kids get the basic financial education. We need more parents to push the school boards to provide more financial education courses.

That’s an important topic, Leo. Unfortunately, I think that in many countries governments don’t think about people really, and financial literacy of population is actually against the interests of those in power. I am sure that when people understand better how they pay taxes, for what, they also become more demanding and in control of how governments then spend their tax payer money.

@Anastasia, I try to avoid talking about politics on my blog, but definitely agree with your view about the government not spending our tax dollar responsibly. I think if government officials’ compensation are tied to their fiscal budgeting performance, our tax dollars will be spent with a bit more prudence.

it’s really different with what i seen . Now only i know we should know clearly about our credit history too!

@Geozo, knowing your credit history and score is important. Keeping a goo credit history and a high credit score is crucial for your financial health.

I think it’s great your provincial government is taking that step. It’s such a shame I wasn’t taught most of this stuff in school. I feel I still have so much to learn when it comes to finances. I hope such a program will come to Quebec too.

@Natalie, depending on the success of the Pilot program in Ontario. Governments are usually copycat organizations and the tend to adopt programs that had been proven to be successful. Hopefully, the program will workout well and Quebec will follow suit.

I’m an American so I am sure out tax shelters and set up are a little bit different. But knowing what little I do about tax issues, we really are very similar with a progressive income tax structure. There is a lot of great information here.

@David, from what I read on other personal finance blogs, the tax system in the US is progressive. To avoid paying more taxes than we need to, we should take advantage of all the tax breaks that our government offers.

Nice information & tips. thanks

@Emilinda, thanks for dropping by and sharing your thought.

This is SOOO true. Great info!

@Jessica, thanks for dropping by and sharing your thought. Hopefully, the info in this post is useful to you.

loving all these valuable tips shared… it is definitely a must read for all…

@Himasnhu, Glad that you find this post valuable to you.

Hi! My brother just recently became a Canadian citizen, so I’ve shared this article with him. I’m honestly a little clueless but the information looks very useful and in depth 🙂

@Namrata, thanks for sharing my post with your brother. Hopefully, the topics in this post can provide him with a starting point to expand his financial knowledge in Canada.

I don’t know what is my credit score (am not sure if here in the Philippines if we have that). However, I have no debts so i think mine is having a good score.

@Blair, I don’t know if the Philippines has any credit bureau companies, but in Canada, we have two. Based on their scoring system, if you don’t have any debt, it’s actually bad for your credit score as you don’t have a history of debt payments.

I think it’s an awesome idea. It’s important to teach kids about how to handle their money especially since they’re going to use those skills when they start earning for themselves.

@Elizabeth, I definitely agree that we should teach our kids money skills and nurture responsible financial management at a young age. I am planning to teach my own kids about money as soon as they are able to understand the concept of money.

Very good analysis, I found your post very useful. I’ll share it with friends with children 😃

@Sara, thank you for the compliment and the sharing of my post. It makes me feel accomplished to know that my posts are making a difference.

Finance always goes over my head. I let my husband do all these stuffs! Tried to understand a few stuff, sounds interesting but again… maybe I’ll pass it on to him 😅

@Tamanna, finance may not be everyone’s favourite topic. If you are not a big fan of money management and your other half can take care of it, then you are in good shape. However, I still believe that two heads are better than one and I would recommend that you work with your husband to plan your finance together as a family.

I wish financial literacy was included in the school curriculum. Everyone needs to know how to handle their finances before they even go out in the real world.

@Peachy, you are definitely right that financial literacy should be included in the school curriculum. Here in Canada, there are a few advocate groups that are lobbying the government to do more on this front. By starting a pilot project to teach kids about money concept is a good start for our school system.

Even managing account and taxes is a complicated subject, I think students also need to have basic knowledge on this.

@Zayani, For people who are reporting their taxes for the very first time, it can be a complicated subject. If we have to file our taxes every year, we should be provided with the basic financial course to teach us how to do it properly.

Thanks for sharing this if not I would not know about these in canada.

@Kelly, Some of the topics such as CPP, RRSP, RESP and OAS are specific to Canada. However, I think that other topics are applicable to other places around the world.

That’s awesome Canada is doing this. I wish the US would do something similar. We need to do a much better job of preparing kids for the real world.

To add to your list, I would teach compound interest and the importance of saving early. I would show an example of how much more you would need to save to reach your goal if you waited to start until 35 as opposed to 25.

@GFY, compound interest and the importance of saving are definitely great additions to the financial literacy curriculum. In my Third Step To Saving A Million Dollars I have demonstrated the power and benefit of compound interest. You’ll end up with almost a 100% more money at the age of 65 if you start saving at the age of 25, rather than 35.

This was such an incredible article! Great information for people like me, I am looking to get a loan to buy a new house, great post

@MaryAnne, it’s great that this article is useful to you. Goodluck in your search for a new house. If you haven’t read it, I’ll definitely recommend my 26 Tips To Buy Your Dream Home With Confidence to help you prepare for your home purchasing journey.

As a fellow canadian I found your article to be really helpful. We actually filled our tax return today. I hope I never have to take out a loan, but thank you for your advice.

@Wanderlust, being debt free is definitely great. However, from a credit history point of view, it doesn’t help you build your credit score. To ensure that you build up a good credit history and credit score, having any bills that you pay in full every month will help. In general, it’s always prudent to keep our credit history in tip top shape because we never know when we’ll need to apply for a loan in the future.

Thanks for the sharing! I never try apply loan before or even credit card >.< I feel there's so much more finiancially knowledge I need to learn =D

@Sharon, Having a credit card is not a bad thing if you always pay your bills on time and in full every month. It’ll help you build up a great credit history and give you more options when it’s time for you to apply for any loans in the future.

I wish the US would also beef up their financial literacy. I feel like most of the literacy is either coming from entertainers or sports figures. Neither of which is real life. I’d love to see some of the charter schools in the US or even colleges demand that financial literacy is taught in order to graduate from high school or college. That would be a wise investment in my opinion.

@MSM, I am not saying that entertainers and sports figures are not qualified to be educators, but the majority of these people in these two industries don’t have a reputable track record when it comes to managing their own finances responsibly. I just hope that governments around the world would do more by providing more financial education to the general population.

I think you and I of are a like mind relative to financial literacy which is an issue in the US just like in Canada. In addition to your list of topics, I would add the introduction to a management tool that actually works. If the tool that is taught is budgeting the program will fail in its key objective … teaching future wage earners how to get the maximum benefit from their income. The Income Companion and Payday Organizer are new programs that establish teachable standards that students can not only learn but will take with them to use for the rest of their lives. I am very interested in your thoughts about the possibility of introducing these new household management tools into high school and college curricula. Thanks.

@George, I’ve always believed that money management skill is a crucial skill that can provide a lifetime of benefits when you’ve learned it. If providing a tool will help people to better understand and manage their finances, I will definite support it. I am always interested to find ways to make things easier for people to learn.

Hi Leo! Thanks for sharing, this is very informative. I have to agree with you, financial literacy and money skills are important to our society and it should be taught in our schools. Every time I am faced with financial difficulties even in as simple as filing tax, I always ask why they didn’t teach us with these things in school. I really hope the government will take a look on this aspect and work on adding financial literacy subject in school curriculum.

I think it’s a great initiative. Financial literacy is very important and if the knowledge is provided in the early age then children will understand its value and it will be a great lesson for their life ahead. This knowledge will help them to take right desition when they will face financial difficulties.

And finally thanks for this valuable article. The ideas and information you have shared here are great. I hope the authority will take the right desition regarding financial literacy.

@Steav, thanks for dropping by. I definitely hope that each level of government would put more emphasis on financial literacy in our school system. I personal think that the education curriculum is not complete unless there is some sort of financial knowledge built in.