Another quarter of the year had come and gone. We’re now into the last quarter of the year and hitting the home stretch of the last quarter of 2017. Before we look too far into the future, let’s take some time to reflect on the our personal net worth review for the latest quarter. As usual, I’ll reflect on the following areas: savings, real estate, debts, investments and net worth.

In addition to reflecting, I believe that it’s also important to do some tax planning as we head into the next quarter. Tax planning should be done throughout the year. If you’ve been doing that, then give yourself a pat on the shoulder for a job well done. If you had been slacking, then the next quarter is the time to take some actions to keep more of your hard earned money in your pocket.

For new readers, the reason that I share my personal net worth review every quarter is to make myself accountable for my financial decisions. I want to encourage all my readers to take control of their personal finance and manage their money responsibly. I believe in transparency, accountability and knowledge sharing. If anyone has any questions, I encourage and welcome any inquiries in the comment section and will try my best to address them.

What’s not my intent is to show off how much money I have or how great I am at managing my money. Please understand that everyone’s financial knowledge, motivation, risk tolerance and life situation is different. The actions that I had taken to improve my finances may or may not be suitable for everyone. The takeaway from my experience is to do whatever that makes sense to your personal situation not because someone else is doing it. So let’s get started.

Savings

From the table below, three out of four of our family saving goals were completed by the end of the first quarter. I believe that when there’s free money available if we save, we should take full advantage of it as soon as possible. The earlier we get the free money working for us, the more time our savings has to grow. These are the reasons why we maxed our Tax Free Savings Account (TFSA) and Registered Education Savings Plan (RESP) accounts at the beginning of the year.

| Items | Target | Amount Saved | Progress |

|---|---|---|---|

| RESP | $5,000.00 | $5,000.00 | 100% |

| RRSP | $17,000.00 | $12,000.00 | 70.59% |

| TFSA | $11,000.00 | $11,000.00 | 100% |

| Vacation Fund | $10,000.00 | $10,000.00 | 100% |

My 2017 family saving goals

The only saving goal that’s currently incomplete on the list is the Registered Retirement Savings Plan (RRSP). We automatically direct 6% of salary straight to our RRSP account for each paycheque. At the end of the year, we also direct any bonuses that we received directly to our RRSP accounts too. With these two actions, it allows us to maximize our RRSP contribution limits every year.

For our savings goals, we will try to complete some goals as earlier as we can. For others goals, we will take the whole year to complete. The important thing to do is to invest often and consistently throughout the year. Pay yourself first and spend what’s left of your income after your savings. Since we have been following the same path for the last ten years, this category is rated as “meets expectation.”

Real Estate

For this quarter, I didn’t do much in this category. It wasn’t the case of laziness. It was a case of wait and see what happens after the government slapped a 15% tax on foreign purchasers in some parts of Ontario. For the last five months or so, there were quite a few events that affected the real estate market, but I was hardly affected at all.

After the 15% foreign tax was implemented in late April, the real estate buyers suddenly disappeared. What was a hot seller’s market, suddenly turned into a buyer’s market. The average home price sold in the Greater Toronto Area (GTA) was at a high of $919,000+ back in April. After four months, the average home price fell to about $733,000. I felt fortunate that I don’t need to sell in this market.

Another event that negatively affected the real estate market was the Bank of Canada raising interest rates twice, a total of 0.5% of increase. Couple that with stricter qualifying requirements on the borrowers and lower appraised values for properties lead to fewer people qualifying for new mortgages. My mortgage was locked in a five-year term, so I don’t have to worry about borrowing or renewing until 2020.

For the value of my real estate properties, I haven’t adjusted the value going up or down for a while. I am content to leave it the way it is. Even with such a large drop in the average price, my estimated value is still below the current market value. In this market, I don’t need to sell and won’t. But if I see any opportunity to buy more properties at a great price, I will be ready to move in. As a result, this category is rated as “meets expectation.”

Debt

In the previous section, I mentioned that the Bank of Canada increased interest rate by 0.50% during the third quarter. That half a percent may not seem like much to the average person. To put it in the perspective of a person who borrows to invest, it really affected my investment rate of return. Since I borrow about $700,000, every 0.25% increase in interest rate, can cost me an extra $1,750 per year. So a 0.50% increase can cost me an extra $3,500 per year. The good news was, I locked in my loans for a five-year term, so the interest rate increase had not affected me yet.

When I took out an investment loan by refinancing my mortgage last year, I didn’t know if the interest will go up or down. The 5-year mortgage rate was 2.59% per year, which was low enough for me. I didn’t care which direction interest was moving so I decided to lock it in for 5 years, which provided me with cash outflow certainty for that period. In hindsight, that was a great decision. Even though there was no activity in this category, but the action I took previously to lock in the interest rate, deserves an “exceeds expectation.”

Investments

Finally, we reached the investment section, the category that I enjoy discussing the most. I have lots to share for this quarter. As I had mentioned early, I will not only conduct a review, but I will also do some tax planning too. My goal is to pay the least amount of income tax as I possibly can, legally of course. So I will break this category into sections: Capital gains, dividends, interest costs and re-balancing.

| Options – Contracts | Ticker | Expiry Date | Strike Price | Premium | Status | Return |

|---|---|---|---|---|---|---|

| Covered Call – 2 | CAT | January 19, 2018 | $110.00 | $628.00 | Active | -181.90% |

| Covered Call – 4 | EXR | September 15, 2017 | $85.00 | $685.03 | Expired | +100.00% |

| Covered Call – 4 | MCD | January 19, 2018 | $140.00 | $765.03 | Active | -714.14% |

| Covered Call – 5 | WFC | January 19, 2018 | $65.00 | $963.77 | Active | +95.34% |

| Naked Put – 3 | BMO | January 19, 2018 | $88.00 | $961.30 | Active | +60.00% |

| Naked Put – 1 | CMG | January 19, 2018 | $360.00 | $961.30 | Active | -110.93% |

| Naked Put – 3 | CNR | January 18, 2019 | $90.00 | $961.30 | Active | -3.03% |

| Naked Put – 5 | ENB | January 19, 2018 | $50.00 | $933.80 | Active | +37.00% |

| Naked Put – 1 | GOOG | January 18, 2019 | $600.00 | $961.30 | Active | +11.79% |

| Naked Put – 1 | GOOG | January 18, 2019 | $850.00 | $961.30 | Active | +10.00% |

| Naked Put – 2 | GS | January 19, 2018 | $185.00 | $1,367.51 | Active | +86.26% |

| Naked Put – 3 | MRU | September 15, 2017 | $38.00 | $361.30 | Expired | +100.00% |

| Naked Put – 5 | V | January 18, 2019 | $70.00 | $961.30 | Active | -1.50% |

| Naked Put – 3 | V | January 18, 2019 | $90.00 | $961.30 | Active | -6.49% |

Options sold during 2017.

Capital Gains

If you had been following my first and second quarter net worth reviews, you’ll know that I had sold quite a few options contracts. Unless I cancel the contracts or the contracts are executed during this year, all the premiums that I collected will be counted as capital gain. The good news is that only half of the value is taxable, but that amount will be taxed at the highest tax rate according to my income. From the table above, the total capital gain for the options premium is about $20,000 and counting. I have a way to offset these capital gains. Read on.

By scanning the return column of the above options table and reviewing the value will not give readers any valuable information unless one understands my principles for trading options. I would recommend readers who are looking for an additional source of income to check out my options trading post to get more understanding of how I make money with options.

Dividends

Not all dividend collected are equal in terms of income tax treatment. Only dividend earned from Canadian eligible companies get the preferential tax treatment (dividend is taxed at a lower tax rate comparing to normal income). This is the reason why my non-Registered investment account is made up of mostly Canadian dividend-paying stocks. For non-Canadian dividends, it’s treated as normal income so it’s not tax efficient.

There is no maneuver to lower your dividend income. However, you do get a (Canadian eligible) dividend tax credit. The amount of credit you get is determined by the amount of (Canadian eligible) dividends that you earned during the year. For me, the total amount of dividends that I collected in my non-Registered investment account for the first three quarters is about $17,000. I can see my tax bill inflating pretty quickly.

Interest Costs

Since I borrow about $700,000 at 2.59% per annum, my interest cost is about $18,130 (=$700,000 * 0.0259) per year. On top of that, I also invest with a margin account for my U.S. stocks and the interest can add up to about $10,000 Canadian per year. Hence, I get to deduct $28,130 off my income at the highest tax bracket. If I can lower my capital gain to about $0, then I will get a huge tax refund (my highest combine tax rate is 43%). The trick I use is in the next section.

Re-balancing

When you buy a basket of stocks, there’s a very high chance that you will have a loser or two in your picks. Even the best stock pickers still have losers in their portfolio so don’t feel bad if you have losers in yours. I also have a few losers too. It sucks when that happened, but it’s unavoidable. Just minimize the number of losers and play the percentage game. If your stock picking success rate is 65% or above, you’re in great shape.

When you have amassed a bit of capital gain like I had for the past couple of quarters, you can sell some of your loser stocks and lock-in the capital losses to offset your capital gains. This is called tax loss selling or harvesting. Here is a previous post that talked about how I used this legal trick to minimize my income taxes.

Now, what if you still believe in the loser stock or still want to invest in the same sector? You still can. For example, I sold my loser stock, Potash Corporation of Saskatchewan Inc. to lock in the losses and I used the proceed to buy Agrium Inc. Agrium and Potash used to be a competitors, but they had entered into an agreement to merge into one company. Hence, I am still in the same sector and will own the combined company when the two companies merged.

I will use this trick to lower my capital gains close to zero every year. This leaves me with all the interest deduction to offset my dividend incomes and to lower my employment income at the highest tax bracket. For the last couple of years, this maneuver had served me very well and provided me with a sizable tax refund. I in turn used the tax refund to further invest. It’s just a cycle of rinse and repeat until I reach a net worth of $2M (63% completed).

Evaluating this category is pretty tough. Based on the first three quarter of 2017, my rate of return is nowhere close to the stellar 12% year-to-date return for the S&P 500 index. It’s more closer to the under performing S&P/TSX Composite index. So this category is definitely “needs improvement” as my investments are under performing.

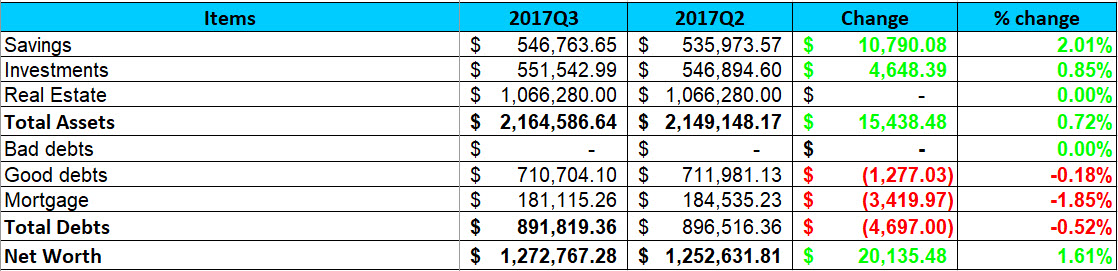

2017 Q3 Net Worth Performance

Net Worth

This quarter has been a bit volatile because my net worth had been up and down right until the last couple of days of the quarter. It has been difficult for me to assess my performance for this category as I don’t really know which direction my net worth will end up with. As of September 28, 2017, I am happy that my net worth manage to gain about $20,000 for the quarter. About 20% of the gain was due to debt reduction.

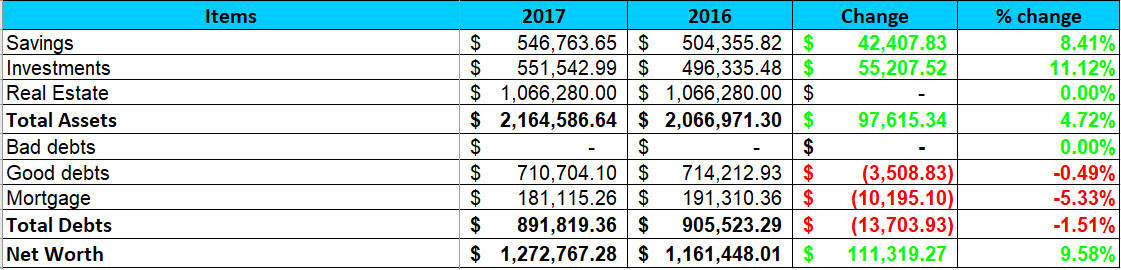

For any quarter that my net worth increased over the previous quarter, I’ll take it. Though the quarterly increase was not as good as the first quarter, I have to be satisfied with a year-to-date increase of over $110,000. In addition, my net worth’s year-to-date increase of 9.58% is very close to my annual goal of 10%. If I can keep on increasing my net worth at a compounded rate of 10% annually, I’ll double my net worth in about 7 years time. So for this category, I’ll rate it as a borderline “meets expectation.”

2017 Year-To-Date Net Worth Performance

2017 Q3 Overall Performance

Overall, this quarter had been a mediocre quarter with lots of volatility in the Canadian stock market. I had been more active than normal when it comes to selling option contracts. I also sold some of my loser stocks in my non-Registered account to offset the capital gains. For the short-term, realizing the losses hurt my wallet, but I will be getting a consolation prize when I file my taxes next April.

At this point, one of my major financial goals is to increase my net worth by 10% annually. For the first nine months, an increase of 9.58% puts me in relatively decent shape and on-track to reach the 10% mark. Hence, a borderline “meets expectation” rating for the overall mediocre performance of this quarter.

So, how often to you conduct your net worth calculation? What financial goals do you set for yourself? How do you balance your current lifestyle with saving for the future?

About Leo

About Leo

Wow you’re doing great so far this year Leo! Thanks for the detailed report. I’ve never tried buying options- looks interesting! I’m going to stick to the index and dividend paying blue chips 🙂

@GYM, I am not buying the options. I am selling them. To me, trading options are like gambling. The one buying the options is making a bet. I am just facilitating (my role is like the house. When it comes to gambling, being the house is better.)

I enjoy reading your blog, admire your investment skills, your diverse selection/portfolio of income streams, the mind boggling leverage/margin, option trades & to see that you are heading in the right direction.

It’s not always getting it right, quarter over quarter things can & do happen. The passive income does not always produce positive returns & that’s OK, it’s upward trend that is key.

So if net worth increases come from income, savings, investments, paying down debt – then when they’re all bundled together to give a positive result, it has to put a smile on your face & encouragement for others.

Seeing the net worth change YOY at almost $112k increase is impressive, as is lowering the debt

Well done Leo

@John, thanks for the kind words. You pretty much summed up what I am trying to do to improve my finance in just a couple of sentences. All the points are spot on. When it comes to growing your net worth, it’s not always just one area that’s doing the heavy lifting. It’s a combination of debt reduction, employment, investment and real income working together.

From quarter to quarter, your net worth may go up or down. The important thing is maintaining a long-term uptrend.

@ Leo, like the lyrics in the song, you are definitely Mr TCB (Takin’ care of business).

I enjoyed reading these reports. I like how you break it down so it’s easy to understand too. My goal for next year is to save a very modest $5,000, but if you knew where I was coming from you’d understand that’s an amazing feat for me!

@Daneen, any financial goal is a great goal regardless of the size of the amount. The importance of our financial goal is to put it down in writing and make ourselves accountable to achieve it. Congrats for making the first step to take control of your finances.

Wow your report is in depth, a great amount of work has gone into compiling it and tracking. You’re an inspiration, thanks.

Wow nice Leo. Great move selling potash and buying agrium too! Your options income is insane. I got to step my game up in that department. 17k in dividends in just your non registered accounts is awesome! Keep killing it man.

I so admire your investment and saving skills! An area I could for sure use improvement. You are really doing a fantastic job not only for yourself but in explaining how you do it! Thank you!

Your authenticity and honesty is refreshing…and inspiring. It has given me food for thought as well. I want to invest in the stock market but it’s overwhelming to know where to begin.

This is really inspiring, I need to look into investing and just finding the right way to do it and not make it be too much for me to handle. Thank you for sharing.

Great investment skills you have. I just wished I had learned this when I was younger.

Thanks for sharing 🙂 Keep up the good wok

THIS IS SO HELPFUL! My hubby and I was just talking about taking control of our financial health.

Learning about savings is really important. Always should be prepared for future.

It looks like you have had another productive quarter. I am working out my finances and know it won’t happen over night bit thankful that I pay more attention to it now.

What a great year and lots of saving and goals you have accomplished. I am trying to do better with my finances so great tips!

I am always impressed about how much work you do with your finances. You are certainly an inspiration to me about how much I can do to manage them and what I should be looking out for. Thanks for the great advice.

Congratulations for gaining this third quarter! I am impressed with your financial skills.