I am a personal finance blogger, a money geek, an investor, a property manager, a diligent saver, an early retiree wannabe or whatever money related personality that I classify myself as it doesn’t really matter. It doesn’t affect my view about money and how I manage it. I think about money on a daily basis and it seems to be hardwired into my thought process. On a daily basis, I try to optimize and improve my finance by asking myself simple personal finance questions.

Some of the personal finance questions can be thought-provoking, some can be inspiring, while others can be a wake-up call. Answering these questions may not be challenging, but taking action to improve your financial situation may be. So without further adieu, let’s see what these questions are and how we can use them to improve our finances.

Do I Earn More Than I Spend Annually?

It’s pretty simple to find the answer to this question. You just add up all of your after-tax pay cheques and subtract all your bills for the year. If the number is positive, then it means that your after-tax earning is more than your expenses. If the number is negative, you have one of two choices. Either earn more money or spend less. Otherwise, a debt spiral will be waiting for you.

Even for the people that are earning more money than they spend, the picture is not as rosy as one may think. According to the Canadian Payroll Association’s survey in 2016, 48% of respondents were living pay cheque to pay cheque. This means only about 52% of people are earning more money than they spend, which leads to the next question.

What Percent Of My Income Did I Save?

According to data from Trading Economics, for the last twenty years, the average Canadian saving rate barely exceeds 6% for any quarter of the year. The worst saving rate was a meager 0.90% in the first quarter of 2005. Let’s think about this for a minute. The average Canadian earned approximately $943 per week, which is just slightly under $50,000 (=943*52) per year based on Statics Canada’s data from 2014. This means that the average person saved at most $3,000 (=$50,000 * 6%) per year based on the average saving rate. With an average salary and an average saving rate, how would the average Canadian be able to afford the average home’s price tag of $478,696 (as of August 2017)?

How Much Was My Discretionary Spending?

We’ve just looked at earnings and savings. Now, it’s time to take a closer look at our expenses per year. Discretionary expenses to be exact. Simply put, discretionary expenses are spending that is in the want category rather than the need category for your day to day needs. For example, these expenses can be vacations, dining out, the daily Latte with your colleague, the golf membership, etc.

Once you add up all of your discretionary expenses, compare that to your savings. If your saving is higher, than you are a diligent saver and are squirreling your way towards achieving financial independence. If your discretionary spending is more than your savings, you are just living your life now and not saving enough for your future. It’s best to lower your discretionary spending slowly over a period of time and direct the extra money towards your savings.

How Much Am I Worth?

To know how much you are worth, you just add up all your assets and minus all of your debts. If this number is negative, then it means that you are deeply in debt. If it’s positive, then it means that you are worth something. Normally, this number doesn’t tell you a lot at any point in time because it’s just a snapshot. If you conduct a net worth calculation over a period of a few years, you should be able to spot a trend in your net worth. Hopefully, your net worth is on an uptrend and it’s growing in the range of 5% to 10%.

How Much Money Did I Make In My Sleep?

The key to achieving financial independence is to have your assets generating income for you passively. You can be worth a million bucks, but if that net worth is not working hard to earn you money, then you’ll most likely have to work for money for the rest of your life. For example, I am worth about $1.2M, but I have about $1.5M in assets working hard to make me more money. Eventually, I hope that my passive income can replace most of my active employment income.

How Much Do I Need To Save In Order To Retire?

Since you have calculated how much money you spent in a year for the first question, you can use that number to find the answer to this question. Most personal finance experts believe that if you saved about 25 times your annual expenses, then you can retire comfortably. Since your expenses are after-tax dollar, I’d recommend using 30 times instead. So if your annual expenses total $50,000 year, you’ll need to have approximately $1.5M (=$50,000 * 30) in savings to retire. (Note: there are CPP and Old Age Security benefits that you were not part of this calculation)

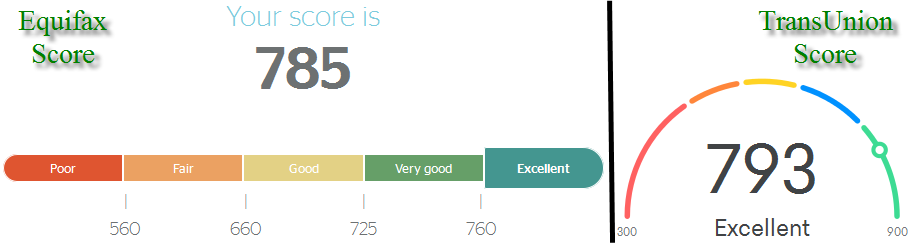

My Equifax and TransUnion credit score.

What’s My Credit Score?

Some people think that their credit score and history are not important and don’t pay much attention to them. We live in a society where borrowing is pretty much a fact of life for most people. Whether it’s a student loan, mortgage, car loan, investment loan, or credit card loan, the higher your credit score, the more negotiating power you have. With a great credit score and history, you’ll most likely be offered better interest rates on your loans. If you are borrowing hundreds of thousands, even a 0.25% discount can mean thousands of savings on interest payments.

How Much Low-Cost Credit Do I Have Access To?

If you have a great credit score and assets, you’ll have great access to low-cost credits like a home equity line of credit (HELOC). You made not need any credit at all or want to borrow any money, but it’s best to have access to credit when you don’t need it. With my credit score and assets, I always have access to at least $100,000 in credit. This allows me to use my emergency fund to invest to earn higher returns rather than keeping them in a savings account that earns me peanuts of an interest rate.

How Much Non-Mortgage Interest Am I Paying?

The ideal answer to this question is zero, with the exception of investment loan interests. Every dollar that you pay in interest that is not tax deductible, it costs you more than a dollar because you pay the interest with after-tax earnings. Hence, to minimize unnecessary costs, it’s best to borrow to invest and buy appreciating assets rather than borrowing for consumption.

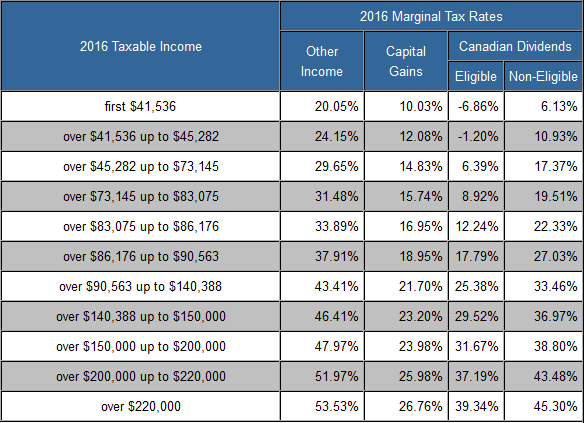

Sourced from TaxTips: Ontario Marginal Tax Rates

What’s My Overall Tax Rate?

Your overall tax rate is the total amount of taxes that you paid as a percentage of your gross income. This number allows to you measure how much money you get to keep for every dollar that you have earned. For example, if your gross earnings were $50,000 and you paid $12,000 in income tax, it meant that your overall tax rate was 24% ($12,000/$50,000). You only get to keep 76 cents of every dollar that you earned. My view has always been, “it’s not how much you earned, it’s how much you get to keep after taxes.” Last year, I kept about 88 cents of every dollar that I earned even though my income range is the 43.41% tax bracket.

How Much Free Money Did I Receive Last Year?

Some people say that there’s no such thing as a free lunch. Well, I think that those people were dining at the wrong restaurants. You can get free money when you save. That was how I got a 72% return on my saving using three simple tricks. You can get free money when you spend or apply for credit cards. Heck, you can even get free money when you shop (using Ebates.ca) or pay your bills (using the Canadian Tire Options Mastercard). If you are not getting free money, you’re missing out.

Why Am I Going To Work?

Most people’s answer to this question is to earn money, pay their bills and put food on the table. There is nothing wrong that. I am doing that too. However, an ideal answer would be, “I go to work because I want to, not because I have to.” How do you achieve this? You can do it by setting a goal to achieve financial independence as early as possible. So going to work will be optional for you one day.

If you like this post, do it to Pinterest or follow me on Pinterest

My Two Cents

Sometimes, the answers to our money questions are there in front of us. It doesn’t take a lot of time or effort to find out the answer to our questions. However, what we do after we have the answers to our questions determines if we will be working for money or have our money working for us in the future.

So, what are your answers to the above personal finance questions? Do you think that by knowing the answers to these questions will help you manage your financial affairs better? Are any of the above questions are thought-provoking, inspiring, or a wake-up call for you?

About Leo

About Leo

“How Much Money Did I Make In My Sleep?” <- Ha! Love this! 🙂

True passive income… sitting and watching investments pay. 😉

@Brad, building a passive income portfolio is great. In about 8 years time, I am hoping to generate enough passive income to never have to work for money again. By then, I will truly be making money during my sleep. 🙂

Very true leo! All great points. In your numbers did you include your primary residence as working for you? Its going up in value too. Just curious if you would or not

@PassiveCanadianIncome, for my net worth, the equity value of my primary residence was included in the calculation. However, for the $1.5M that’s working to earn me money, no. The reason that I have more money working to earn me money is due to leverage. For example, if you buy a rental property for $500,000, I only put in about $125,000 in equity, but I have the full amount working to earn money for me.

This looks like a very helpful post in answering some of my own personal financial questions. I don’t consider myself a financial blogger but your tips could help me none the less.

I work very hard and every time I think I am going to save money, one of my kids has a crisis and I shell out the money needed to help them. I really need to get on track for retirement savings.

@Jen, I think that helping your kids out is great. If your kids are adult-age, I would tell them the assistance is in the form of a loan and they need to pay you back. If you don’t set the expectation that it’s not free money, the first thing they will do is to come to you when they are in financial trouble. Kids need to learn how to table responsibility for their finances.

Love all these points and when I turned 40 and realized that when it was time to retire, I was not going to be in a good place. Don’t wait until you are 40 to start saving for retirement. Its too easy today to save. Great points.

@ Tammy, it’s never too late to start accumulating wealth, whether it’s passive income, extra/invested income to live on or into or to reach for retirement. I know many folks that had zero when they started collecting social security, then by the time they were 70 they had double the amount of income that the government was paying them.

Leo is a prime example of how to do it, mind you it’s not everyone’s cup of tea.

Starting with just $100 from zero to getting $1000/mth income within 60 months is possible….right Leo?

@Tammy, you’re right. It’s never to too late to save regardless what age you are at. Ideally, everyone should start at a young age so that their money has time to grow.

@Leo +1 for this weeks post. It all seems so simple & relative when you write it in your blog

Just make sure there is money for Mexican food !

@John, you’ve made my day. I am glad that you’ve enjoyed this post. I love food. I not only want to have enough money for Mexican food, I want to have enough money to try any food I want :).

These are great questions to ask yourself and do it annunally to control your spending and budgeting. These are a great way to prepare for retirement.

These are all great questions to consider. My husband is very financially minded and I really appreciate his expertise in this area.

A 30 times multiplier on expenses seems like a very conservative approach to retirement. I have heard percentage of final income used with numbers between 9-14 times. Looking at the numbers assuming 100K income to make math easy. In this scenario you take home about 70K after taxes (30% tax rate assumed). Assuming a 6% savings rate means you are spending 94% of your take home pay (i.e. expenses) or 68.5K. Given these two numbers, here is the resulting savings.

scenario a) 30X expenses = 30 * 68.5K = 2,055

scenario b) 14 X final income = 14 * 100K = 1400K

This is a pretty big difference. The 30X final expenses should be able to pay for 30 years of living assuming that you make the dubious choice of storing the money in your mattress. If you keep the money working for you and compounding you shouldn’t need as much. Even if I think the 30K multiplier is conservative, I like the concept of focusing on your expenses to retire instead of your earning. This allows you to retire based on saving money OR reducing expenses.

@Jenn, your expenses is a reflection of your everyday life. Hence, using your expense numbers to estimate your retirement need is a much more accurate estimate. Secondly, using your income to estimate introduces an uncertainty such as income taxes. Your income is before tax money and your spending is after-tax money. As a result, 30 times your annual expense is a very conservative estimate and we will most likely have more than enough money to last a lifetime.

I need to get on with savings, these points are really great and just made me start questioning even more than I thought. I guess it’s time to check myself and answer all these questions for myself.

These are great questions, Leo. Though I’m not asking all of them, they are all aligned with my personal goals. Meaning, I’m taking action in all of these areas, but I’m not consciously asking these very good questions on a regular basis. Instead, I sort of set it and forget it. I save and invest automatically. I pay my bills automatically. I go to work automatically (I’m blessed with a great job I enjoy, fortunately). And I focus on building my side-hustle so that one day I will be able to work because I want to, not because I have to. If I’m not asking these questions regularly, I think it would be very beneficial to ask them at least annually. Thanks for the suggestions!

@Tanya, I’m a finance nerd (and I must admit that I am a bit obsessed with managing my money). Asking these finance question once in a while is sufficient for the average person.

I like that you are automating your saving. I love the concept of paying yourself first. Great job!

You offer some valuable Financial advice here that I have been trying to stress to all my boys. Since they won’t listen to me, because I am Mom, I’m going to share your article with them. Perhaps hearing the same Financial recommendations for Success coming from someone else might hit home with them. Thank you so much!

@ChrissyAdventures, I know how you feel as a parent. Most kids don’t like to take advice from their parents. I am one of those kids, lol. Hopefully, this article can help your kids see that you want the best for them and had their best interest at heart.

I think we all have to make decision on whether we want our money to work for us or spend more time making it.

These are great tips for keeping yourself in check! I need to crack down on discretionary spending!

Sondra xx

prettyfitfoodie.com

I love this post because it really puts things in perspective. My family and I are just now starting to live comfortably. We are nowhere near ready for retirement however. My hubby is a spender and I am a saver so it’s kind of hard to get him to stash money away for the future. I’m going to show him this post!

@Melanie, It’s definitely difficult to save money if one of the spouses is a spender. To turn a spender to a saver takes time, effort and baby steps. Start with saving small amounts and then gradually increase. Over a period of a couple of years, once the spender starts to build the money discipline, saving will become easier. Good luck.

Those are some great points and this can be quite handy in the future. We aren’t near retirement zone yet but that doesn’t stop us from saving money in case of emergencies.

We got to the point in our lives that we work when we want to. It has been amazing. We have very few bills and the only reason we work is to save for the next holiday.

@Wanderlust, reaching the milestone of working when we want to is a great achievement. I am about eight years away and I can’t wait to discover that feeling.

I really need to think about making sure I lower my discretionary spending and save up for bigger things that I need with more money in savings. I don’t think I will be able to save a ton but there are things I can do.

I like the question of “am I making money in my sleep!! There’s a quote by Warren Buffett on the internet that says “If you don’t find a way to make money while you sleep, you will work until you die.”

@GYM, that’s a great quote from Buffett. Every quote he said is so simple and beautiful.

One of the reasons that I wanted to achieve financial independence as early as I can is because I don’t want to “work until I die.” Life is too short to work till you die lol.

Yes! Knowing the answers to these questions obviously helps me manage my financial affairs better! Thank you for a very interesting read!

Definitely think those questions are important for us to ask ourselves. They’re thought-provoking and most importantly they can help us manage our finances better. Sometimes we’re in situations coz we don’t take the time to think about things.

I’m a spender and thanks goes to my husband for being our saver and being so good with money! This is def helpful advice, will share it with him too.

These are all helpful tips. I love the idea of making money while I sleep. After reading this I realized that I have not given attention to passive income. I want to learn more on this.

These are really good questions especially if you’re spending more than what you’re bringing in. I’m really trying to get a hold of my finances now.