I’ve always believed that “there’s such a thing as free lunch in this world, you just need to be lucky and skillful enough to find the restaurant that offers it.” In my money saving post, I’ve listed the methods that I used to either save or get free money. For this post, I am going to describe in further details on some of the methods and show you how I saved money, get free money, compound the free money on top of my savings to get even more free money. I am going to show you how I started with $12,000 in savings, but end up getting $20,500 in my saving accounts and $160 extra to take my wife out on a date night (Shhhhhhh, she doesn’t know about the date night yet.)

Step #1: Contribute to my employee share ownership plan (ESOP)

One easy way to start saving for retirement is to contribute to your RRSP. If you set up an automated withdraw for every pay cheque from the start of your employment, you’ll hardly notice any material impact on your daily finance. As I mentioned in my money saving post that I was lucky enough to get a 50% matching for every dollar that I contributed to my ESOP. In this case, I contributed $5,000 and got $2,500 free money. Remember, the key thing is to direct both your contribution and the matching to your RRSP account. This way, you get to lower your income by the contribution amount (you don’t pay tax on the last $5,000 of your income – the highest tax bracket) and all your money get to grow tax-free until you withdraw.

Step #2: Maximize my RRSP contribution

There are three ways that I used to conquer this task. First, using the automated withdraw method for every pay cheque. I killed two birds with one stone by having the ESOP contribution count toward my RRSP contribution amount and getting free cash along the way. The second way is to direct my year-end bonus towards my RRSP account. By doing that, I am adding that amount to my RRSP contribution amount and my bonus money is not getting taxed when it’s paid to me and it gets to grow tax-free until I withdraw. The third method is to top up the remaining amount to maximize the contribution before the March 1st contribution deadline. The first two methods did most of the heavy lifting, so I rarely need to do much for the third method. So maximizing my RRSP contribution is about an additional $7,000 on top of my ESOP.

Step #3: File your tax early to get your tax refund early

I usually file my tax around mid-April or so. My highest tax bracket was 43% (darn, that’s a lot of taxes to be paying. On the bright side, I also get a lot in refunds too if I have deductions) for last year. So with the $12,000 being tax-free at 43%, I get about $5,160 in tax refund just from my RRSP contribution alone. Sweet.

Step #4: Use my tax refunds to contribute to my kids’ RESP account

Since I am getting a free $5,160 in tax refunds, I don’t have to find extra money somewhere to contribute to my kids’ RESP. All I need to do is contribute $2,500 per kid, the government will provide a free education savings grant of 20%. So I contributed a total of $5,000 for both of my kids to get $1,000 in free money. Extra icing on my saving cake.

If you like this post, feel free to share and Pin it to Pinterest.

Step #5: Compound the savings

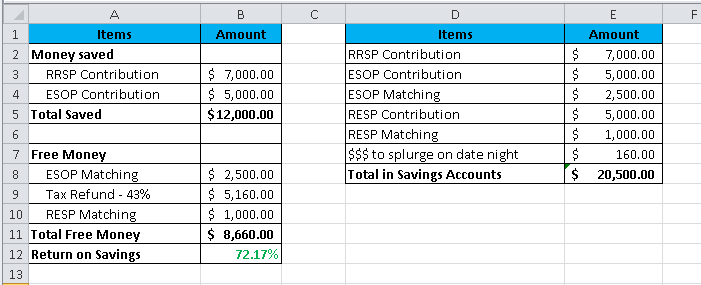

So when I add everything up, I saved a total of $12,000 ($5,000 in ESOP and $7,000 in RRSP). I am getting a total of $8,660 in free money ($2,500 in ESOP matching, $5160 in tax refunds and $1,000 in RESP grants). At the end, my saving account is a whopping $20,500. That’s an awesome return of 72% right off the bat. See the breakdown summary in the tables below.

My two cents

I think that saving money is great, but getting free money on top of your savings is even better. I am not that great of an investor, but when I get a 72% return to start off with, that’s like getting to start at the 50-meter line when you are running the 100-meter race. This is an advantage that I can easily and legally gain and I might as well use it to my benefit.

So, what easy methods do you use to get free money and compound the return on your savings?

About Leo

About Leo

That is incredibly impressive that you have been able to build a net worth of a million dollars over a ten year period. I’m guessing when you can earn 72% return on your money that is one way to accelerate your net worth 🙂

Congrats on the awesome job so far and keep up the awesome work!!!

Hi MSM,

To be honest, the steps that I take is not complicated at all. Information about retirement saving plans, and education grants are all over the news every march and April when it comes to tax time. For me, I know that there is a limit to how much I can make in a year. Also, it’s not that easy to make money in the stock market. So the best option for guarantee instant income is free money and that is the first and safest place to look for returns for my money when I save.

Once again, thanks for dropping by. I really appreciate you taking the time to share your thoughts.

Just by taking advantage of three incentives and you are able to increase your savings by 72%, I am surprised at why wouldn’t more Canadians take advantage of free money. Great job with taking full advantage of these offers. If only more people pay closer attention to the power of compounding.

As I mentioned in my bio, I want to show people how to save money in a disciplined way. I am pretty sure that most people know about these offers, but being able to take advantage of it and control one’s own spending is something that’s difficult for people to master. So by showing people real examples, I hope that I can encourage and motivate more people to save.

The numbers are so simple, yet it’s very elegant. Three simple savings and you get 72%. Thanks for providing the motivation. The numbers helped a lot.

You have done so great! You don’t mention TFSA’s but I think they are an essential tool as well. Do you agree? I am encouraging our University aged kids to max out their TFSA’s while living at home and saving their RRSP room for when they are making more money… is that good advice? I think saving from a young age is the best way to make a good start. I admire your technique and it obviously worked well for you. I love the idea of using tax return to fund the RESP’s … great way to save!

Hi Lori,

I think you are catching on. The point of this article is to demonstrate that anyone can compound their savings by just starting with three simple saving strategies. I do in fact use the TFSA and it’s a great tool. My TFSA contribution limit is max every year.

The advice to start investing at a young age and have their money compound in a tax shelter account is very sound. I couldn’t have said it better myself.

This is impressive. Its amazing what you can do with a little research and discipline. We area a military family enrolled in the TSP program where money is taken out automatically every month for the last 20 years. I will say that we have increased the amount over the years to its max and that grows very fast. Our intention was to buy a small house with mostly cash so we could retire and do whatever we want. We will have that and more when its all said and done as well as a retirement paycheck and other investments. And we did this without fancy or expensive financial assistance.

@Stacey, just by reading your thoughts, I think that you too have a very disciplined saving habit. The fact that you are able to buy a house with cash is also quite impressive too. I really admire people who can save in a very disciplined manner.

I can tell this post was well researched and written.. thanks for sharing your valuable information with us all!

@Thecla, it really pays to do your research when it comes to free money from the government. Once you’ve discovered the savings, you can use it year have the year. That’s the beauty in know the tax rules.

I need to work harder at saving money. I really like the idea of getting free money on top of my savings and need to follow your tips to get ahead. Have fun on your date.

@Terri, getting feel money is the top motivator to save money for me. It can also be a motivator for you too as the tax rule can be applied to anyone. All you have to do is find the rules that gives you the most benefit.

The is something I need to start focusing on more. I started financial planning a little late and have some time to make up for.

@Gina, it’s never too late to start financial planning and saving for the future. Time will always be your investment best friend if you have a long term outlook.

This is really helpful, useful advice. I’ll be following up on a few points.

Ooh that is a handy tip, it is definitely a good idea to file your tax return early so you don’t have to wait or in case you forget. Putting a note to do that for future reference x

Three simple steps and 72% savings?? woww i have to do some serious financial planning now . thanx for sharing 🙂

This is so interesting. I will have to keep this in mind because I don’t know a lot about this.

Wow you’ve done an amazing job finding ways to build your savings – and FAST! I’m impressed – I can’t believe that was all in just one year!

This is impressive! There’s really nothing better than being able to save while also getting free money in the process. This is a very smart use of your money. Good job!

Three simple steps only? That is amazing! I really need to look at my finances now.

http://www.lovekimber.com/

Great post! I think my hubs is doing the same thing when it comes to filling taxes. We also use Child care benefit and church donations for our tax return. But I usually leave tax filing to him.

Nice one! It’s important to stay on top on finances and investments. I need to make more use of the tax-free ISA (UK) than I currently do. Every bit counts 🙂

@Nadine, one of my secrets to achieving a accelerated saving is to take advantage of tax free accounts and getting free money from the governments when I save money. If you can take advantage of it, you definitely should.