During my university days, I came across a wealth accumulation concept called the Smith Maneuver, which allows the investor to borrow money from the built up of equity in the investor’s home to invest. As we all know, any loan that an investor (in Canada) took out to earn an income, the interest payment on the loan is tax deductible. So in this post, I’ll show you the steps that I’ve taken to use the Smith Maneuver to borrow $50,000 to build a stock portfolio that will generate a positive cash flow for the first 5 years of my investment.

Step #0: The prerequisite

To use my primary residential home as a collateral to borrow more money, I definitely need to own a home for a period of time and have been paying down my mortgage or the value my house had appreciated in value. Lucky for me, both scenarios occurred because I live in Markham, Ontario and I do have equity built up in my house. Therefore, I will have no issue borrowing money from the equity of my house.

Step #1: Taking out the loan

There are two ways that you can take out the loan, either through a Home Equity Line of Credit (HELOC) or refinancing your mortgage. I chose the refinancing route as it gives me more advantages when it comes to executing my investment strategy. First of all, when you borrow money from the HELOC, the interest rate is Prime plus 0.5% or more, which comes to more than 3%. Secondly, the interest rate is variable on the HELOC, which means my investment cost will rise if the interest rate rises. On the other hand, when I refinance my mortgage with a five year fixed term, my investment cost will stay the same for the five full years. I can also, lengthen the amortization of the mortgage to lower my monthly payment, which will have minimal impact on my monthly mortgage payments. Based on today’s rate at Rate Hub, I can get a five-year fix rate mortgage for about 2.35% annually. However, the current rate for my loan is 2.59%, so I use the higher rate for my $50,000 to demonstrate the strategy.

Step #2: Invest the proceed

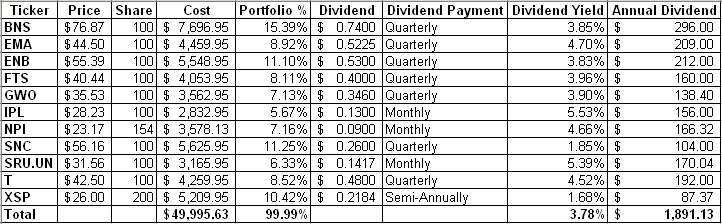

Based on the day that I drafted this post (December 09, 2016), I assumed that I can buy all the stock/ETF in my portfolio on the Toronto Stock Exchange at the closing price of that day and each transaction costs me $9.95. From the table below, you can see that the average dividend yield of my portfolio is about 3.78% or $1,891.13 in dividends. The total cost of my stock portfolio is about $49,995.63.

Step #3: Calculate my annual cash flow

Since I took out the loan at 2.59% per year, the annual interest cost of my $50,000 loan is $1,295 (=$50,000 * 0.0259) per year. From a straight calculation, I am getting an annual dividend of $1,891.13 and minus the interest cost of $1,295, the net result of my loan is about $596.13 cash going into my pocket every year. However, I am living in Canada and I won’t be able to avoid paying taxes. So the next step will be to calculate the after-tax result of the cash flow.

Step #4: Calculate the after tax result

With interest cost, every dollar that you pay, you can deduct it off the highest tax bracket of your income tax. In another word, my highest tax bracket is 43%, so I get $556.85 (= $1,295*0.43) in tax refunds. On the other hand, the dividends that I get will be income, so it’ll be taxed. However, dividend income is being taxed preferentially at only about a 33% tax rate, which amounts to $624.07 (=0.33*$1,891.13). Hence, the total after tax result of my $50,000 investment loan is $528.91 (=$1,891.13 – $1,295 + $556.85 – $624.07) of free money every year for the fist first five years. Just a note, if the dividend payment goes up or down, then my net result will be affected positively or negatively.

My two cents

When it comes to investment, not everyone will have the same risk tolerance and knowledge to invest by themselves. However, the basic principle to making money is knowing how to take advantage of opportunities and structuring your investments in a way that will give you a better chance to succeed. The key thing is to only invest in what you know and comfortable with. The example that I showed is only one of the methods used for the Smith Maneuver. You can also use the same process to invest in real estate instead of stocks.

So which method do you use to get free money when you borrow?

About Leo

About Leo

Wow this is incredibly interesting and not something that I have explored. This is definitely something that I will need to read up more and see if it makes sense for me. Thanks for opening my eyes and sharing!!!

With interest rates so low, if you have the means to borrow money cheaply and the investment skills and knowledge to make more than the interest expense, you’ll be ahead of the game. The good news is, any money that you borrowed to earn income, you get to deduct 100% of the interest cost at the top of your marginal tax rate. This is what high income earners use to make more money. I am glad that you find is helpful.

Recently, I have been considering if I should use my home equity to invest in a rental property. What’s holding me back is the thought that if I get a bad tenant and causes damage to the property, then I will get a lot headaches as I am not much of a handyman at all.

The handyman issue is an easy problem to solve. You can partner up with someone who as renovation skills. I partnered up with my buddy to run our rental property and it had been a great success since day one.

Bad tenants is a tough one to master. I tried to screen my tenants with reference checks, income, guarantors and credit checks. Even with this, it’s still no guarantee that the tenant is good. However, with those these, I weeded out quite a few of them. That’s all you can do.

Let’s say that in five years, the stocks that you choose stays flat or goes up, you make money. What if it goes down, then you will loose money. If that is the case, what would you do?

Wow! what an eye opener! I am not comfortable with that type of risk but glad to see it spelled out… thanks! At this stage of our life, I feel like we need to build slowly on what we have but then again, we lived through the downturn 10 years ago or so and I won’t forget that awful feeling of losing money every month for quite a while on our small investments!